UK CBAM: The UK's Carbon Import Levy

What businesses need to know about the UK's Carbon Border Adjustment Mechanism

Trusted By

Industry Leaders

Industry Leaders

What is the UK Carbon Border Adjustment Mechanism?

The UK CBAM (Carbon Border Adjustment Mechanism) is a significant step towards achieving the UK’s decarbonisation goals and combating climate change.

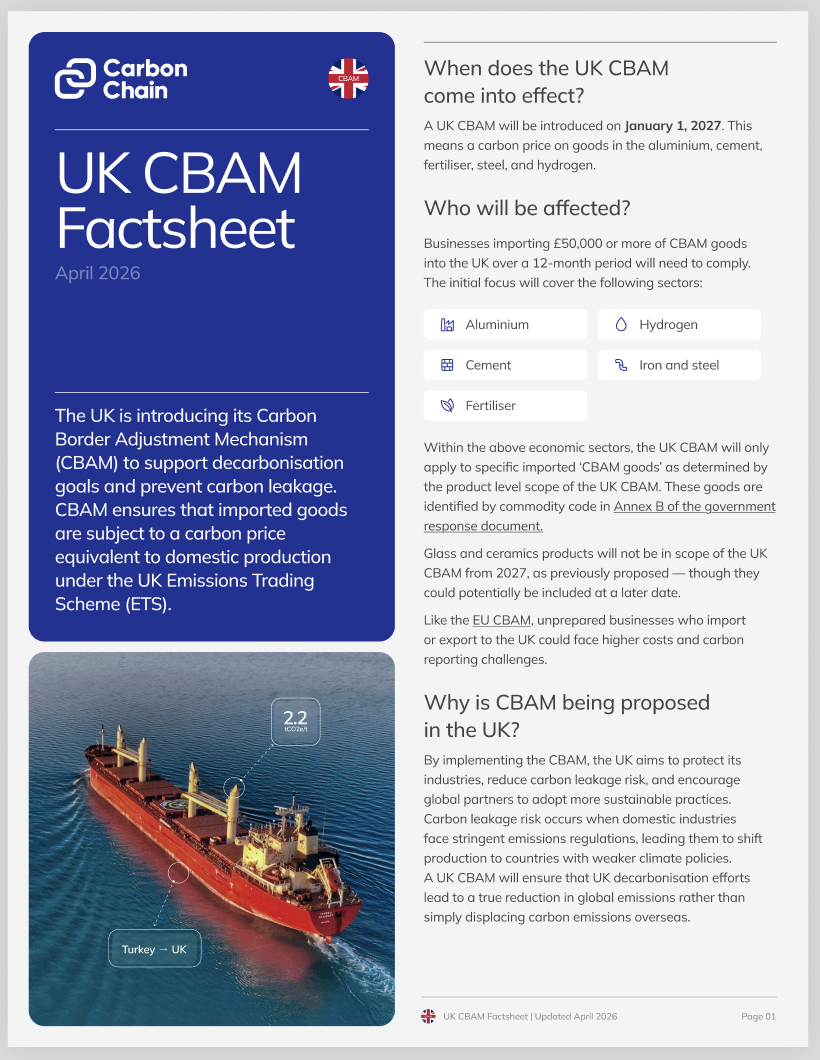

UK CBAM date is confirmed as January 1, 2027. This means a carbon price on goods in the aluminum, cement, fertilizer, steel, hydrogen, iron, and steel sectors. Only businesses importing £50,000 or more of CBAM goods over a 12-month period will need to comply (an increase from the previous minimum threshold of £10,000).

By implementing the CBAM, the UK aims to protect its industries, reduce carbon leakage risk, and encourage global partners to adopt more sustainable practices. Carbon leakage risk occurs when domestic industries face stringent emissions regulations, leading them to shift production to countries with weaker climate policies. A UK CBAM will ensure that UK decarbonisation efforts lead to a true reduction in global emissions rather than simply displacing carbon emissions overseas.

Goods imported into the UK from countries with a lower or no carbon price will have to pay a levy by 2027.

On October 30, 2024 the UK announced key updates to its approach to CBAM:

- Verifiers already accredited under the EU CBAM regime can operate under the UK CBAM without obtaining separate UK accreditation. This significantly reduces the compliance burden for installations that export to both the EU and UK.

- Therefore installations that have already undergone EU CBAM verification can use the same verifier and, in many cases, the same verification process to satisfy UK requirement.

- UK has no transitional period.

- Legal Mechanism: UK CBAM means tax, while EU CBAM uses certificates.

- It won’t include glass and ceramics products, as previously proposed, due to feasibility concerns that were raised during the consultation process from March 21, 2024 until June 13, 2024.

- UK has record retentions of 6 years (EU has 5 years)

- System boundaries for all goods are identical (EU and UK)

- The legislative process for UK CBAM is underway, with the second tranche draft has been released. Consultations are expected to conclude in May, 2026.

Like the EU CBAM, unprepared businesses who import or export to the UK could face higher costs and carbon reporting challenges.

LEARN MORE

Get a detailed breakdown of the CBAM reporting requirements for importers (declarants) and sellers (installations).

Download our UK CBAM factsheet

When is CBAM being implemented in the UK?

The UK Carbon Border Adjustment Mechanism (CBAM) will be introduced January 1, 2027. Initially, the UK government committed to an implementation as early as 2026, but updated the timeline following its public consultation.

Which sectors will UK CBAM apply to?

The UK CBAM is designed to tackle the most carbon-intensive industrial goods imported to the UK, putting a carbon price on products in the aluminum, cement, fertiliser, hydrogen, iron and steel sectors.

Within the above economic sectors, the UK CBAM will only apply to specific imported ‘CBAM goods’ as determined by the product level scope of the UK CBAM. These goods are identified by commodity code in Annex B of the government response document.

Glass and ceramics products will not be in scope of the UK CBAM from 2027, as previously proposed — though they could potentially be included at a later date.

How is UK CBAM liability calculated?

Legislative process of CBAM UK

Following a consultation process that ran for 12 weeks and received over 340 responses from stakeholders including UK and overseas industry, trade associations, importers, think tanks and academics, the UK government responded with an effective mechanism that aligns with the nation’s climate goals.

- Returns and payments will be due 5 months after the end of the first accounting period — 31 May 2028. The quarterly deadlines from 2028 are also now published in a detailed table (e.g. Q1 2028 return due 31 July 2028).

- During the first calendar year of CBAM, businesses will have until 31 January 2028 to register rather than the standard 30-day window. This is practically important for compliance planning.

- The April 2026 legislation that the government will set out full verification guidance in due course. But Verifiers already accredited under the EU CBAM regime can operate under the UK CBAM without obtaining separate UK accreditation. This significantly reduces the compliance burden for installations that export to both the EU and UK.

LEARN MORE

Get a detailed breakdown of the CBAM reporting requirements for importers (declarants) and sellers (installations).

Download our UK CBAM factsheetAbout the latest UK CBAM consultation

On 9 April 2026, HMRC published draft secondary legislation covering the next tranche of UK CBAM rules. This follows the first 2026 consultation, which covered administrative requirements, the CBAM rate, and carbon price relief for goods that have already borne carbon taxation in their country of origin.

This second consultation sets out how embedded emissions will be calculated, what records must be kept, and how emissions data must be monitored and verified. It is directly relevant to UK importers of aluminium, iron and steel, fertilisers, cement and hydrogen, and to the overseas manufacturers supplying them.

The consultation closes 21 May 2026.

Default values and the first illustrative CBAM rate are both expected to be published by HMRC in Autumn 2026, ahead of the 1 January 2027 go-live.

What this means in practice

While default emissions values will be available for businesses that cannot yet access actual supplier data, those default values are set deliberately high meaning businesses that rely on them will pay more than they need to. Understanding your actual embedded emissions, and being able to verify them, is where the financial difference gets made.

Compliance ultimately rests on three things: knowing which goods are in scope via commodity code, having reliable emissions data for those goods, and filing accurate quarterly returns from 2028 onwards. The sooner businesses have that infrastructure in place, the better positioned they will be when the tax applies from 1 January 2027.

CarbonChain Connect is built to support all three. Want to explore our product?

Past consultations for UK CBAM

March–June 2023: Carbon leakage measures consultation

A consultation ran from 30 March until 22 June 2023. The UK government published a consultation document and factsheet on measures to mitigate future carbon leakage risk, which included potential policies such as the overarching pricing mechanism, mandatory product standards, demand-side policies promoting low-carbon goods, and an embodied emissions reporting system. On 18 December 2023, the government published its consultation outcome following over 160 stakeholder submissions.

March–June 2024: CBAM design and administration consultation

The consultation ran from 21 March 2024 to 13 June 2024 and sought views on the design and administration of UK CBAM from importers, their agents, tax advisers, trade bodies and other interested parties including those overseas. The government published a consultation document and outcome summary following over 340 responses. Key outcomes included confirming 1 January 2027 as the go-live date, raising the minimum registration threshold from the proposed £10,000 to £50,000 over a 12-month rolling period, and removing glass and ceramics from the initial scope.

February–March 2026: First draft secondary legislation consultation

This technical consultation ran from 10 February 2026 to 24 March 2026 and covered the first tranche of draft secondary legislation. The draft regulations covered administrative requirements such as information required on registration, record keeping, and valuation of CBAM goods; calculation of the CBAM rate and availability of carbon price relief including verification requirements; and reimbursement arrangements. The draft also proposed that a trial CBAM rate be published in Q4 2026 to allow businesses to prepare. The outcome of this consultation is pending, with the government reviewing responses ahead of laying final secondary legislation later in 2026.

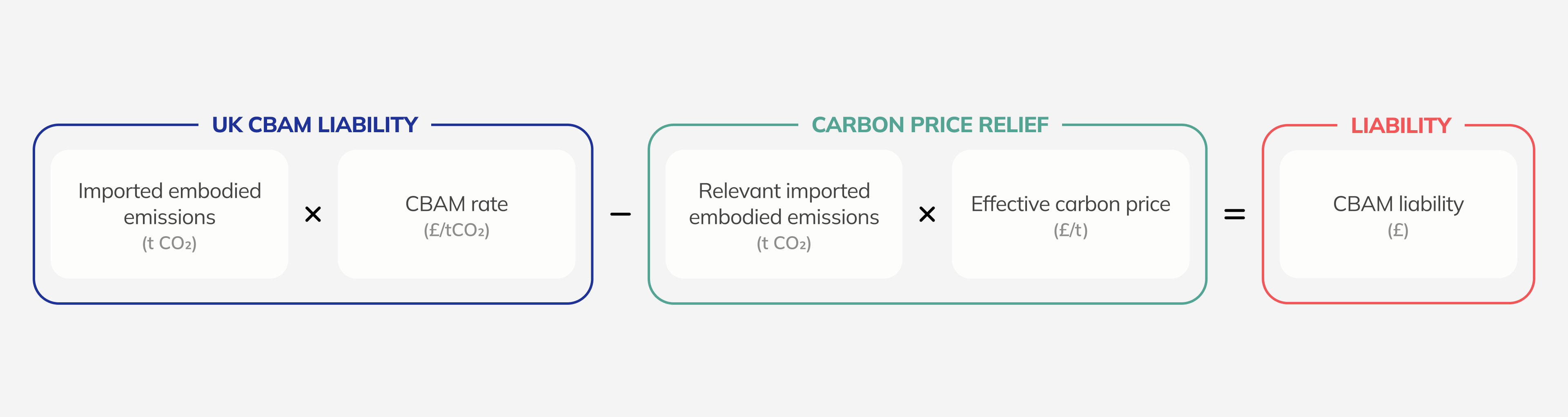

How is the UK CBAM calculated?

The calculation of the UK CBAM liability will center on the carbon footprint of imported goods, with importers required to pay a carbon price that bridges the difference between the UK’s carbon pricing mechanisms and any explicit carbon price paid in the country of origin (if applicable). Implicit carbon pricing will not be recognized.

The UK CBAM is set to work in the following way:

- The tax point arises when a CBAM good is imported into the UK and becomes liable to import duty. For goods not subject to import duty, the tax point occurs when the goods enter the UK. The new language for this ties it specifically to import duty liability rather than “customs controls”.

- For goods exported under the outward processing; if the original good was a CBAM good that was of UK origin and/or subject to a carbon price in the UK, the carbon price previously incurred can be used to adjust the CBAM liability down. Only the difference in value between the original good and the processed CBAM good will count towards the £50,000 minimum registration threshold.

- For CBAM goods originating outside the UK and re-imported using the returned goods relief the April 2026 legislation adds an important additional condition. There will also be no CBAM liability for Union goods exported from Northern Ireland into the EU and reimported into the UK providing the goods are reimported within 3 years of export from Northern Ireland and returned in the same state in which they were exported. Where all conditions are met, the returning CBAM good will not need to be declared on a CBAM return or be factored into the calculation for the £50,000 minimum registration threshold.

- Individuals will not need to register or account for CBAM if the total value of their CBAM goods passing a tax point is below a minimum threshold of GBP 50,000 over a rolling 12-month period.

- Those liable will be required to submit a CBAM return and pay the due amount at the end of each accounting period. The first accounting period will cover imports from January 1 to December 31, 2027, and subsequent periods will be quarterly from 2028 onwards.

- The CBAM rate will be adjusted quarterly, reflecting the average UK ETS price over the prior quarter. There will be an adjustment to account for the allocation of Free Allowances (FAs) under the UK ETS. This FA adjustment will be based on a sectoral average of emissions covered by FAs over a baseline period, adjusted annually by a reduction factor to reflect the phase out of FAs under the UK ETS. Importers will self-assess their liability by:

- Multiplying the total emissions per type of good by the applicable UK CBAM rate, and

- Deducting any explicit carbon price already paid in the country of origin, provided that it meets the UK’s definition of an explicit carbon price (such as carbon taxes or emissions trading schemes)

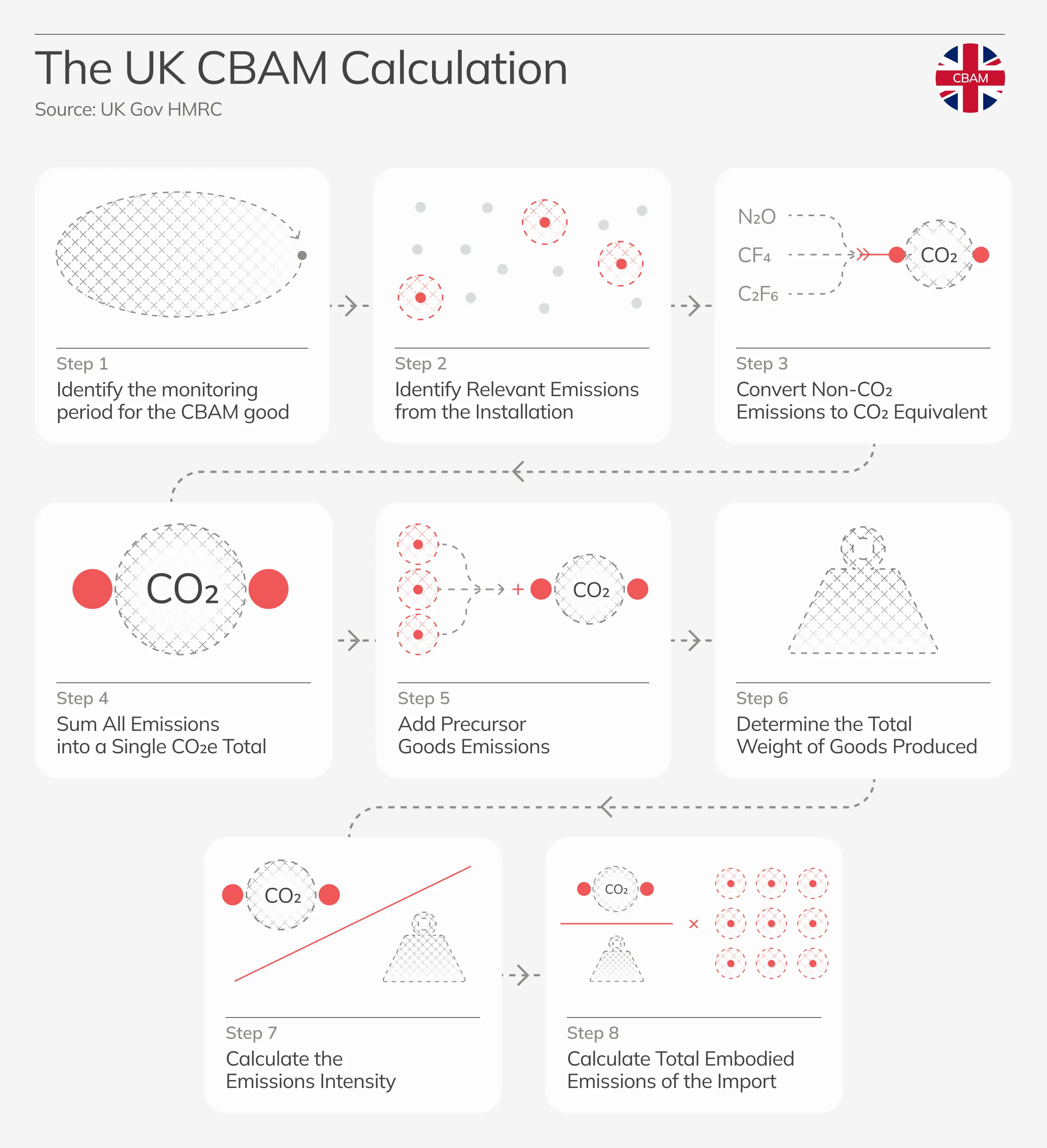

- The UK CBAM will apply to direct emissions only. Direct emissions are those from production processes, including emissions from heating and cooling, whether produced on-site or off-site.

- Importers have two options to determine the emissions embodied in imported goods for CBAM liability calculation:

- Actual emissions data: Verified data on the actual emissions generated during production, which aligns with EU requirements and is preferable where available.

- Default emission values: Government-provided default values calculated based on average emissions by product type and key trading partners. From 2027, the government will proceed with a single default value set per product. The methodology for calculation will be confirmed and published in advance of the CBAM introduction in 2027. Default values will be set for an initial period (2027-2030) and will undergo a review before potential adjustments are implemented from 2031 at the earliest.

The first CBAM accounting period will cover imports from January 1 to December 31, 2027, with subsequent quarterly periods beginning in 2028. During the first calendar year of CBAM, businesses will have until 31 January 2028 to register rather than the standard 30-day window. This structured approach aims to ensure that imported goods meet the same carbon standards as those produced domestically, fostering a level playing field and incentivizing lower-carbon imports.

Returns and payments will be due 5 months after the end of the first accounting period — 31 May 2028. The quarterly deadlines from 2028 are also now published in a detailed table (e.g. Q1 2028 return due 31 July 2028), which would be useful to reference.

LEARN MORE

Get a detailed breakdown of the CBAM reporting requirements for importers (declarants) and sellers (installations).

Download our UK CBAM factsheetHow do companies prepare for CBAM in the UK?

Companies can prepare for the UK CBAM and stay competitive in the UK market by:

- Conducting a thorough assessment of their carbon emissions;

- Implementing measures to reduce their carbon footprint;

- Partnering with lower-carbon suppliers;

- Investing in cleaner technologies.

Companies can prepare for the CBAM by using CarbonChain to measure the emissions embedded in their imported products and the carbon intensity of supplier facilities, as well as identify lower-carbon suppliers.

Download the factsheet

X